Birla Niyaara

Worli — the strongest fundamentals in South Mumbai · RERA P51900031916 (T1) · P51900054455 (T2·Silas)

The strongest fundamentals in South Mumbai — freehold land, a listed promoter, the most disciplined RERA filing, and a genuine 70%-at-OC payment structure — wrapped around punishing surroundings.

The SHORTLIST rests on the best paperwork you'll find here — freehold, listed-company title, the most disciplined RERA filing, no floor inflation, and a genuine 70%-at-OC payment structure. What you accept in return is the surroundings: a 33,000 sqm commercial estate hidden on the compound and set to grow, the worst connectivity in South Mumbai, three mega-developments closing in, and a marketed sea that's largely blocked. The fundamentals are the strongest here; the context is the trade — and note this analyses Silas (Tower B), not the topped-out Tower A. Rexray’s FVL (Fundamentals · Value · Livability) index frames the call; the verdict is yours.

Fundamentals

7.8/10StrongPillar score is the average of the scored attributes below; some attributes are qualitative and carry questions rather than a number.

- This is the best title in the portfolio: freehold land (that land parcel, ~57,500 sqm) owned by the listed company ABREL, with no government-landlord or renewal exposure.

- The earlier Wadia-family dispute over the adjacent parcels is settled by consent terms (closed).

- The only frictions are a two-lender No-Objection Certificate needed for pre-possession resale, and the standard '30-acre' marketing overstatement of the estate's size.

- Confirm the freehold extent and the two-lender NOC process for a pre-possession resale.

- Delivery has real strengths: strong sales, clean listed-company funding, and a genuine deferred-payment structure (70% due only at Occupancy Certificate).

- The caveat is which tower you're buying — the analysed unit is in Silas (Tower B), which is only about ten floors up; Tower A is the topped-out one.

- Registered possession is March 2029 against a marketed Dec 2028.

- Note too that the clubhouse and a planned future tower depend on a pending MCGM land amalgamation, because the plot's floor-area is exhausted.

- (How we score this: filing frequency, document legibility and up-to-dateness on the RERA website, then specific flags.)

- This is the most disciplined RERA filing in South Mumbai — complete, fresh and well-organised.

- One structural note: the brand is Birla Estates, but the entity that signs (and that recourse runs against) is the listed parent, Aditya Birla Real Estate (ABREL).

- This is Birla Estates' first luxury large-scale residential project, so there's no comparable delivered record to grade yet — judge it on the documented facts and the listed parent's standing.

- The main brochure-vs-reality gaps are scale and contents: the marketed '75 storeys' is Tower A (not every tower — the analysed Silas is 44), and a 33,000 sqm commercial estate on the compound is absent from the marketing.

- Confirm which tower, its sanctioned floor count, and what's sanctioned to rise toward your facing.

- Which tower am I buying, and its exact sanctioned floor count — the 75-storey figure is Tower A, not every tower.

- What's the registered area of this specific project vs the wider Century Mills estate?

- Confirm the commercial estate footprint and where it sits.

- What's sanctioned to rise toward my facing over the next 5 years?

Value

7.7/10StrongPillar score is the average of the scored attributes below; some attributes are qualitative and carry questions rather than a number.

- On the analysed Silas (Tower B) unit, south is the genuinely clear aspect (a band-7 view).

- The marketed west is largely screened by Sugee Marina Bay across the tower's height (it's a 44-floor tower, and the screen runs below ~F45).

- The good news, against earlier framing: the north is open — Niyaara's own third tower sits well north toward the Development Plan road, at enough distance that it does not wall the north aspect.

- What's sanctioned to rise toward my specific facing over the next five years, and is my south sightline protected?

- On the analysed Silas unit, efficiency is a strong 88% with a Separate Servant Entry, but it lives a little flat: a single south aspect with weak cross-ventilation, and a modest 3.2m ceiling.

- Efficient and well-proportioned, but not as airy as the best in South Mumbai.

- The exposed-face glass specification is the open item.

- LES from floor plan: 88% → 8.5 · registered documents

- vs 12ft luxury benchmark: 3.2m → 5 · Rexray analysis

- Separate Servant Entry: yes (Tower B Silas) → 9 · Rexray analysis

- which way the home faces (from the floor plan): S single (weak cross-vent) → 5.5 · Rexray analysis

- Quality of Window/Railing Glass (Glazing, Heat Trapping, Brand) — buyer question: PENDING · Rexray analysis PENDING

- The west-face glass specification — brand, glazing thickness, and the heat-trapping (SHGC / U-value) number.

Clean — there's no foyer or 'private lobby' Non-RERA-area trap. You own everything you pay for.

- from the agreement / floor plan: None · registered documents PENDING

- carpet sqft: 3887 · registered documents

- bmc enforcement: none · Rexray analysis

- fsi to legalise: None · registered documents PENDING

- The analysed unit (TB-3104, Silas) registered at about Rs.30.7 crore — roughly Rs.78,900 per sqft on carpet.

- The market here is tight (limited committed inventory), and because the layout is an efficient 88%, your effective rate on usable area stays close to the headline carpet rate — you're not paying much for dead circulation.

- What is the all-in cost — including stamp duty, registration and goods-and-services tax (GST)?

- What is the rate on the area I actually own (carpet plus deck) versus the marketed area?

- What have recent apartments in this building / micro-market actually registered at?

Livability

6.1/10FairPillar score is the average of the scored attributes below; some attributes are qualitative and carry questions rather than a number.

- There's no rehabilitation housing on the plot — a clean residential cohabitant profile.

- The offset is commercial: about 33,000 sqm of it (a ~9-floor retail tower plus the existing Birla Centurian office) shares the compound, driving weekday footfall, parking and water draw, and it's absent from the marketing.

- And it grows — ABREL's own 10-acre northern parcel (~42,000 sqm residual) is most likely to add further commercial and residential, so the on-compound density is on an upward trajectory.

- The large land area dilutes it, but it's a real and rising load.

- rehab: none · registered documents

- BN-F05, flagged IPD driver: 33,347 sqm · registered documents

- retail tower: ~9 floors (Wing TC) · registered documents

- birla centurian: existing office (Wing B) · registered documents

- mhada sublot: 3.24 ac, government · registered documents

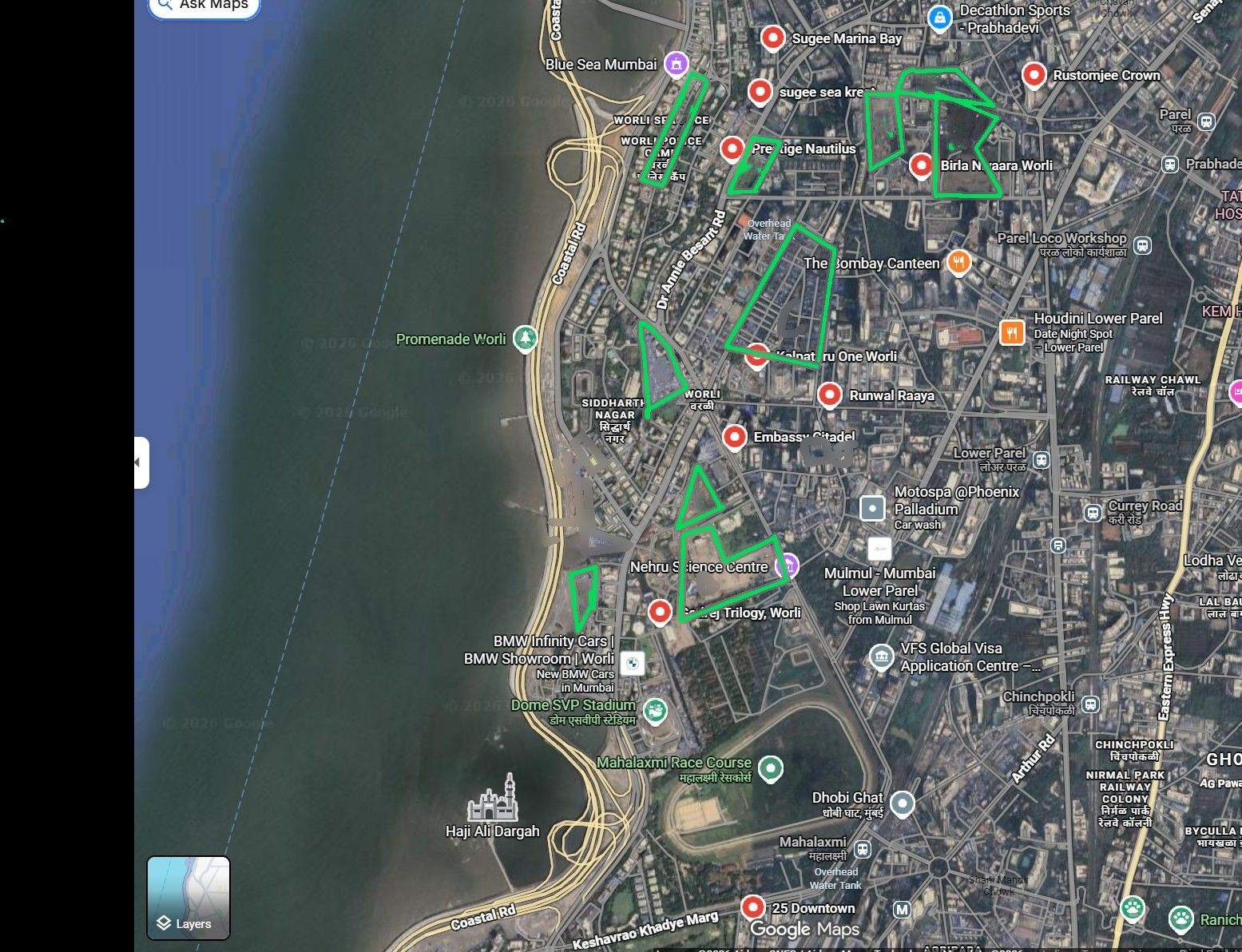

- Pandurang Budkar Marg is already saturated (Lodha Park, Ikea, Kamala Mills, Raheja Altimus, Omkar SRA all feed it), and three mega-developments are closing in: Sumitomo's 22-acre estate to the east, ABREL's own 10-acre parcel to the north, and a Lodha ~4-acre parcel north of the Development Plan road.

- The dominant harm here is density and a choked road — the surroundings are being reshaped over the next decade.

- sumitomo: 22ac ~1M+ sqm GFA · registered documents

- abrel north: own 10ac parcel · registered documents

- lodha 4ac: ~4ac parcel · registered documents

- road: PB Marg — choke (Lodha Park/Ikea/Kamala Mills/Raheja Altimus/Omkar SRA) · Rexray analysis

- Connectivity is the worst in South Mumbai.

- It's about 22 minutes to the coastal-road on-ramp at 11am today, and it degrades toward 28–33 minutes by 2032 as Pandurang Budkar Marg — already at the limit — absorbs the Sumitomo development on the same route.

- On a worked example, the last-mile out can take longer than the Sea Link ride itself.

- GMaps 11am -> Godrej Bay View: 22 min · Rexray analysis

- road headroom: PB Marg choke + Sumitomo 22ac on the route; worked example: last-mile > the Sea Link ride · Rexray analysis

- directional band, not a measured future time: x1.3-1.5 · Rexray analysis PROJECTION

Kitchen ventilation passes cleanly: a dedicated chimney exhaust to the outside (kitchen to a utility with an external window), across all four unit types.

- kitchen→utility→external window, all 4 unit types: PASS · registered documents

- Lift provisioning is strong on both towers.

- Silas runs four homes per floor on six passenger lifts for a peak interval of about 20 seconds — Grade A.

- The topped-out Tower A (a 78-floor tower on seven passenger lifts plus a service and a fire car) is also Grade A at about 25 seconds, borderline only at the slowest assumed speed.

- from total floors − podium: 40 · registered documents

- passenger lifts: 6 · Rexray analysis

- units per floor: 4 · Rexray analysis

- ≈ ceiling + slab: 3.7 · Rexray analysis assumption

- spec unconfirmed — sensitivity band: 4–6 m/s · Rexray analysis assumption

- Water adequacy passes on the conditions we can see, with no charge escalators.

- The open question is the large commercial estate's water draw, which isn't yet quantified against the parent approval — confirm the commercial provisioning is sized, and this firms up further.

- The agreement's car-park schedule names the type outright: tandem bays in the second basement, allotted through the society after conveyance.

- You drive to them, but two-deep means the inner car is blocked until the outer one moves.

The podium is shared with a retail tower, so also check how visitor and retail traffic mixes with resident parking.

Rexray's database will, over time, be enriched with the attention to detail and quality ethos of each builder. For now, below is the checklist you should verify with the builder before you decide.

- Who's the architect, and what comparable have they delivered?

- Do the lobbies need lights during the day?

- Gym/pool/lobby sized for how many residents? (gym sqft / residents)

- Does this unit's layout meet your Vastu requirements (entry, kitchen, master)?

- Can a fire tender or an ambulance reach the lobby?

- Who is actually building it?

- Mivan or conventional — and how are the tie-holes grouted and cracks controlled?

- What's the realistic floor-cycle, and how does the monsoon factor in?

- Which steel/cement? Facade glazing spec? MEP contractor? STP/solar?

- Which marble/fittings exactly? Which window system? VRV brand?

- Deck/bathroom waterproofing system? How's the facade sealed into the structure?

- Gypsum or block internal walls — and are the party walls insulated?

- Does the back-up generator power my whole flat, or only the common areas?

- Is the parking solo, tandem, or a mechanical stack — and how wide are the bays?

- On a field read, the Silas tower is a homogeneous, high-end, large-unit profile — a single owner-occupier gentry, no rehab cohabitants.

- The community variable here isn't the building; it's the growing commercial estate and the surroundings around it.

- What is the ticket-size range in the building — the gap between the cheapest and the most expensive home?

- Is the building vegetarian-only, or skewed to a single community?

- Is it owner-occupied, or investor- and tenant-heavy?

- What is the pet policy?

Findings register

31 findings · severity-rankedEvery marketed claim set against the documented fact, sourced. Critical and high first.

- The MCGM amalgamation status of that land parcel/1546 — and the fallback for the clubhouse and Tower TD if it isn't approved.

- ABREL's committed programme for the 10-acre northern parcel (~42,000 sqm residual) beyond Tower TD.

- A written commitment not to invoke the agreement Clause 29: that clause lets the land owner change the floor count and building programme AFTER you've signed — get it in writing that they won't use it to alter what you bought.

- The south-face sightline and Quality of Window/Railing Glass (Glazing, Heat Trapping, Brand) for the specific floor you're considering.